The Poor Man's Covered Call Explained

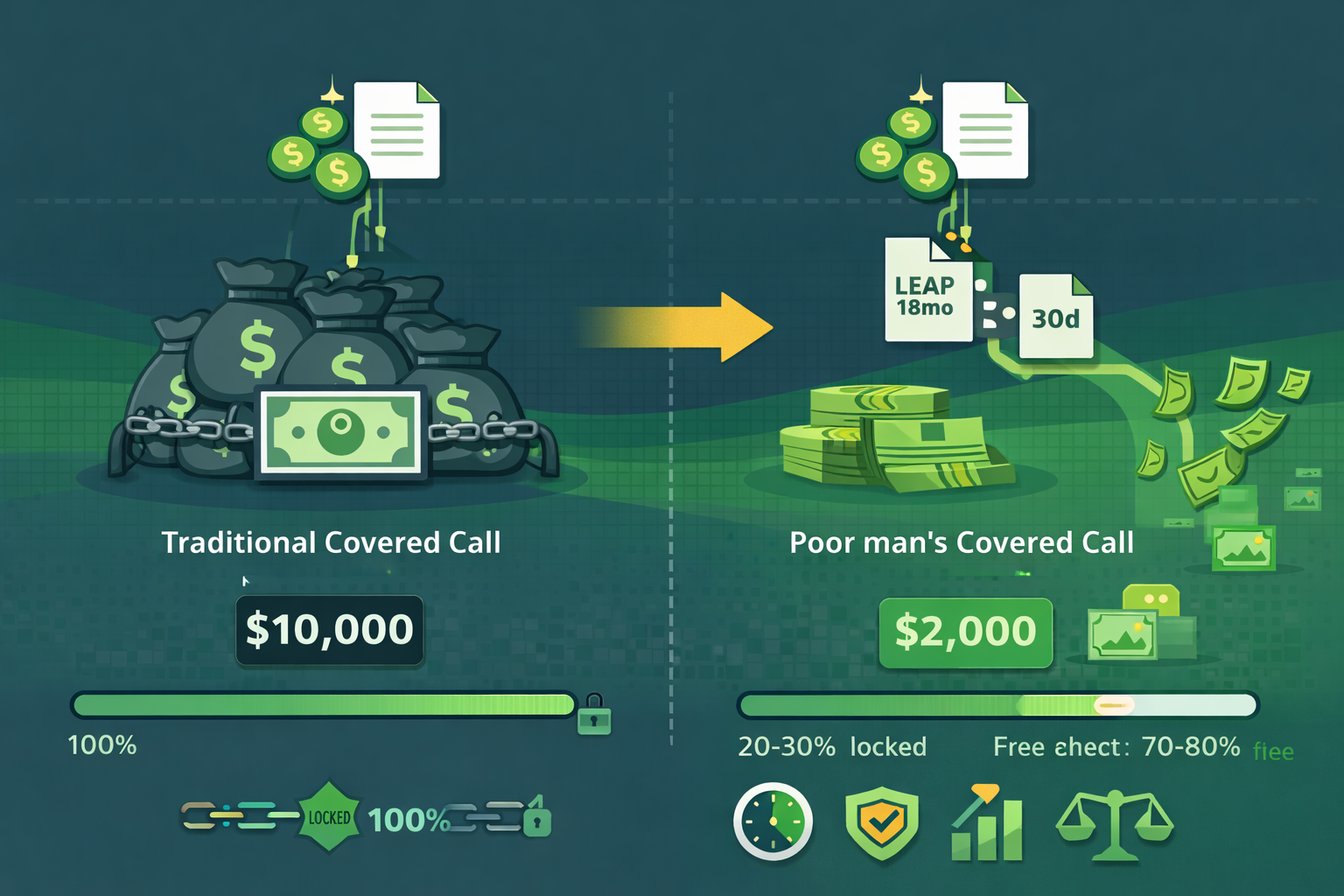

Covered calls generate steady income, but they lock up capital. You need $10,000 to control 100 shares of a $100 stock. The poor man's covered call solves this by replacing stock ownership with a long-dated LEAP, then selling short-term calls against it. Same income potential, 70-80% less capital required. Here's how it works and when it makes sense.

TL;DR

- Replace stock with a LEAP: Buy a deep in-the-money call (delta 0.80+) with 12-18 months to expiration instead of owning shares

- Sell calls like normal: Sell short-term out-of-the-money calls (30-45 days) against the LEAP to generate income

- Capital efficiency: Control 100 shares for $2,000-3,000 instead of $10,000, freeing capital for other positions

- Same income mechanics: Collect premium just like a regular covered call, but with leverage and lower upfront cost

- More risk, more reward: The LEAP decays over time (theta), so you must be right about direction and timing, not just patient

What Is a Poor Man's Covered Call?

A traditional covered call means you own 100 shares of stock and sell a call against them. If you own "QualityCo" at $100 per share ($10,000 total), you might sell a $110 call for $2 ($200 premium). Your max profit is $1,200 if assigned ($10 stock gain + $200 premium). Your downside is the full $10,000 if the stock crashes.

A poor man's covered call (PMCC) replaces the stock with a LEAP, a long-dated call option. Instead of buying 100 shares for $10,000, you buy one LEAP contract with a $90 strike, 18 months to expiration, trading at $15 ($1,500 total). This LEAP has a delta of 0.80, meaning it moves $0.80 for every $1 the stock moves, almost like owning shares.

Now you sell a $110 call (30 days) for $2 ($200 premium), just like a covered call. Your cost basis is $1,500 instead of $10,000. You just freed $8,500 to invest elsewhere. Same premium collection, same upside mechanics, but with one key difference: the LEAP loses time value (theta decay) over 18 months. If the stock goes sideways or down, you lose more than a covered call would.

Step-by-Step Mechanics

Let's walk through a real example with QualityCo trading at $100.

Step 1: Buy the LEAP. Look for a strike at least 10-20% in-the-money, meaning the strike is below the current price. For QualityCo at $100, you might buy the $85 strike LEAP expiring in 18 months. Cost: $18 per share ($1,800 total). Delta: 0.85 (moves like owning 85 shares).

Step 2: Sell a short-term call. Sell a 30-45 day call at a strike above the current price. QualityCo at $100, sell the $108 call for $2.50 ($250 premium). This is your income.

Step 3: Manage like a covered call. If QualityCo stays below $108 at expiration, the short call expires worthless. You keep the $250 and sell another call next month. If QualityCo rises above $108, your LEAP gains value (delta 0.85 means a $10 stock gain equals $8.50 in LEAP gains). You can close the short call, roll it, or let it get assigned and sell the LEAP.

Step 4: Repeat monthly. Each month, collect $200-300 in premium by selling new calls. Over 12 months, that's $2,400-3,600 in income on a $1,800 investment. Annualized return: 133-200%, assuming the stock stays flat or rises modestly.

Risk: If QualityCo drops to $90, your LEAP loses value. The $85 strike LEAP might drop from $18 to $12 ($600 loss). Covered call holders would lose $1,000 ($10 per share on 100 shares), but they still own shares that can recover. Your LEAP has an expiration clock. If the stock doesn't recover before expiration, you lose the time value permanently.

Capital Efficiency Explained

The big advantage: you control the same exposure with much less money. This lets you diversify or hold cash for opportunities.

Example: You have $30,000. Traditional covered calls on three stocks at $10,000 each locks up all your capital. With PMCCs, you spend $2,000-3,000 per position, controlling three stocks for $6,000-9,000 total. You still have $21,000-24,000 in cash to deploy on value opportunities, protective puts, or more LEAPs.

This flexibility matters during market volatility. Cash is optionality. If QualityCo drops to $80, you can buy shares or sell puts to average in, something you couldn't do if all your capital was tied up in stock.

The cost: LEAP theta decay. Every month, your LEAP loses a bit of time value. For an 18-month LEAP, theta is small (maybe $0.05-0.10 per day), but it adds up. If the stock goes sideways for 12 months, you might collect $3,000 in premiums but lose $500-800 to theta. Net: still profitable, but less than a covered call that has no theta drag.

When to Use a PMCC

Poor man's covered calls work best in specific scenarios:

Strong conviction on direction. You believe QualityCo will rise from $100 to $115+ over the next year. A PMCC lets you amplify gains and collect income along the way. If you're neutral or bearish, stick with cash-secured puts or regular covered calls.

High implied volatility. When IV is elevated, short-term call premiums are juicy. You collect more income per month, offsetting theta decay faster. In low-IV environments, premiums shrink and the strategy loses appeal.

Capital constraints. You want exposure to five wonderful companies but only have $50,000. PMCCs let you control all five for $10,000-15,000, leaving $35,000-40,000 for other opportunities. Without PMCCs, you'd only afford two or three positions.

Undervalued stocks with catalysts. QualityCo trades at $100, fair value $130, and earnings growth is accelerating. A PMCC gives you leveraged exposure plus income. If the stock re-rates to $125 in 12 months, your LEAP gains $20+ ($2,000+) plus $2,500-3,000 in call premiums. Total: $4,500-5,000 on a $1,800 investment (250% return).

Don't use PMCCs if:

- You're bearish or expect the stock to stay flat for years. Theta decay eats returns without compensating gains

- The stock has low liquidity or wide bid-ask spreads on options. You'll lose money on execution

- You're new to options. PMCCs require managing two positions (long LEAP + short call) and understanding Greeks. Master covered calls first

- You can't afford to lose the LEAP premium. PMCCs are leveraged, losses hurt more than stock ownership

Managing the Position

Roll the short call monthly. Each month, close the expiring short call (buy it back) and sell a new one 30-45 days out. This generates consistent income and keeps your LEAP protected from assignment.

Adjust for valuation changes. If QualityCo rises to $115 (near fair value), stop selling calls or move strikes higher. Don't cap upside when the stock is still undervalued. If it drops to $90, consider rolling the LEAP to a lower strike or longer expiration to reduce cost basis and extend time.

Exit before expiration. Don't hold the LEAP to expiration. With 3-6 months left, theta accelerates (time decay speeds up). Close the LEAP, take profits or losses, and either move to a new LEAP or switch back to stock ownership.

Hedge with protective puts. If you're worried about a crash, buy a protective put on the underlying stock (e.g., $90 put for $2). Costs $200 but caps downside on the LEAP. Now you have income (short calls), leverage (LEAP), and insurance (protective put). This triples complexity but makes sense for concentrated positions.

Example: 12-Month PMCC Performance

QualityCo starts at $100. You buy the $85 LEAP (18 months, $18 per share, $1,800 total). You sell monthly calls at $108-110 for $2.50 average ($250/month).

Scenario 1: Stock rises to $120. Your LEAP gains $17 (from $18 to $35, delta 0.85 means $20 stock gain = $17 LEAP gain). You collected $3,000 in premiums over 12 months. Total gain: $3,000 (premiums) + $1,700 (LEAP appreciation) = $4,700 on $1,800 invested (261% return). Covered call would have made $2,000 (stock gain) + $3,000 (premiums) = $5,000, but on $10,000 invested (50% return).

Scenario 2: Stock stays at $100. Your LEAP loses theta, maybe $800 over 12 months. You collected $3,000 in premiums. Net: $2,200 profit on $1,800 invested (122% return). Covered call would have made $3,000 on $10,000 (30% return).

Scenario 3: Stock drops to $85. Your LEAP drops from $18 to $8 ($1,000 loss). You collected $3,000 in premiums. Net: $2,000 profit on $1,800 invested (111% return). Covered call would have lost $1,500 (stock drop) but kept $3,000 in premiums, net $1,500 profit on $10,000 (15% return).

Scenario 4: Stock crashes to $70. Your LEAP drops from $18 to $2 ($1,600 loss). You collected $3,000 in premiums. Net: $1,400 profit on $1,800 invested (78% return). Covered call would have lost $3,000 (stock drop) but kept $3,000 in premiums, breakeven.

Notice the pattern: PMCCs amplify gains when stocks rise or stay flat, but they protect less on the downside. The LEAP can go to zero. Stock can recover forever.

What Could Go Wrong?

- Theta decay eats returns: If the stock goes sideways for 18 months, time decay can cost $1,000-1,500, erasing much of your premium income

- Directional risk: PMCCs require the stock to rise or stay flat. If it drops hard, you lose capital faster than a covered call

- Assignment complexity: If your short call gets assigned, you don't own shares to deliver. You must close the LEAP and settle in cash, creating tax events and execution risk

- Liquidity issues: Wide bid-ask spreads on LEAPs or short calls can cost $50-100 per trade, killing profitability on small positions

- Overleverage temptation: Because PMCCs use less capital, it's tempting to overextend. Five PMCCs on shaky businesses is riskier than two covered calls on wonderful companies

Mitigation: Only use PMCCs on high-conviction, wonderful companies with liquid options. Size positions so that losing one LEAP doesn't hurt your portfolio (max 5-10% per position). Track theta daily. If decay exceeds income by more than 20%, close the position and reassess.

Next Steps

- Learn when advanced strategies like PMCCs make sense

- Understand LEAPs as a stock substitute before using PMCCs

- Master rolling techniques to manage short calls

- Review covered call basics

- Explore protective puts to hedge PMCC risk

Poor man's covered calls are powerful when used right. They free capital, amplify returns, and generate income just like regular covered calls. But they add leverage and theta risk. Use them on wonderful companies you're bullish on, with liquid options, and only when you have the experience to manage two moving parts at once. When in doubt, owning shares beats owning options.

*Disclaimer: This content is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own research before investing.*