Advanced Time Decay Management

Time decay is your secret weapon if you're selling options, and your silent enemy if you're buying them. Most investors treat theta as background noise, but advanced value investors optimize it. They sell options at the steepest part of the decay curve to maximize income, and buy options where decay is slowest to preserve value. The difference between ignoring theta and managing it deliberately can add 2-5% annual return to an options-enhanced portfolio.

TL;DR

- Theta accelerates in the final 30-45 days: Sell short-term options to capture the steepest decay curve for covered calls and puts

- Theta is slow beyond 90 days: Buy LEAPs or long options where time works slowly, preserving extrinsic value

- Layer expirations: Stagger covered calls across weekly, monthly, and quarterly cycles to smooth income and reduce timing risk

- Avoid the dead zone: Options with 45-90 days to expiration decay moderately, neither fast enough to sell aggressively nor slow enough to buy safely

- Monitor theta per position: Track daily theta decay for each option to see how much income you're collecting (or losing) just from time passing

What Is Theta and Why It Matters

Theta measures how much an option's value declines each day, assuming nothing else changes (no price movement, no volatility shift). For option sellers (covered calls, cash-secured puts), theta is income, you collect premium as time passes. For option buyers (LEAPs, protective puts), theta is cost, your contracts lose value daily.

A $5 option with 0.05 theta loses about $5 per day in time value. If you sold that option, you pocket $5 daily (scaled by the number of contracts). If you bought it, you're paying $5 per day for the privilege of holding it.

Key insight: Theta isn't linear. It accelerates as expiration approaches. An option with 180 days to expiration might lose $3/day, while the same option with 30 days loses $10/day. Advanced investors exploit this curve by selling short-term options (fast decay) and buying long-term options (slow decay).

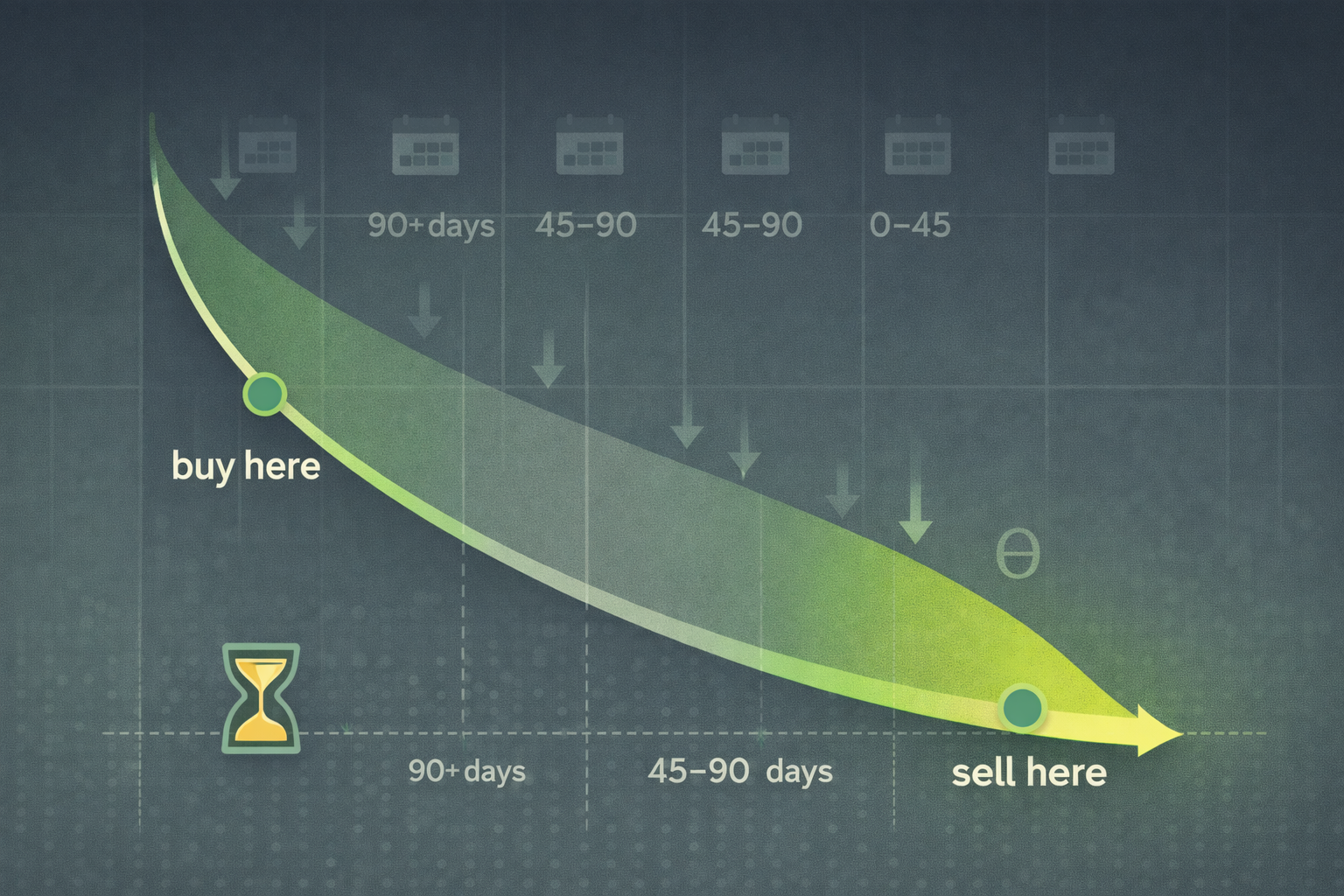

The Theta Decay Curve: Three Zones

Think of time decay as a ski slope:

- Slow decay (90+ days to expiration): The top of the slope. Options lose value gradually. This is where you buy LEAPs or long protective puts

- Moderate decay (45-90 days): The middle. Decay speeds up but isn't dramatic. This is the "dead zone" where trades often make little sense

- Steep decay (0-45 days): The bottom. Theta accelerates rapidly. This is where you sell covered calls and cash-secured puts for maximum income

Example: A $5 call option with 120 days to expiration loses about $3/day. The same option at 30 days loses $10/day. The same option at 7 days loses $15/day. Selling at 30-45 days captures the steepest part of the curve without risking weekly expiration chaos.

Selling Short-Term Options for Maximum Theta

Covered calls and cash-secured puts generate the most income when sold 30-45 days before expiration. This is the "sweet spot" where theta decay is fast, but you still have enough time to roll or adjust if needed.

Let's say you own "QualityCo" at $100 and want to sell covered calls. You have three choices:

- Weekly option (7 days): $1.50 premium, 0.20 theta/day. Fast decay, but you'll need to roll every week, creating transaction costs and decision fatigue

- 30-day option: $3 premium, 0.10 theta/day. Optimal decay rate, you collect $3 every month with one decision

- 90-day option: $5 premium, 0.05 theta/day. Higher total premium, but slower decay means less income efficiency per day

The 30-day option wins because it captures theta at the steepest part of the curve. You earn $3 in 30 days, about $36 annualized (on a $100 stock, that's 36% annual yield from premiums alone, though assignment risk caps upside).

Pro tip: If volatility is high, extend to 45 days to collect more premium. If volatility is low, stick to 30 days to avoid tying up the position unnecessarily.

Buying Long-Term Options for Slow Decay

When buying LEAPs or protective puts, you want the opposite: slow theta. Options with 12-24 months to expiration lose only $2-4 per day, giving you time for the business to compound without bleeding premium.

Let's say "QualityCo" trades at $100, and you want LEAP exposure. You compare two strikes:

- 12-month LEAP, $90 strike: $18 premium, 0.04 theta/day. You pay $18 upfront but lose only $1.20/month to decay (0.04 × 30 days)

- 6-month LEAP, $90 strike: $12 premium, 0.06 theta/day. You pay $12 upfront but lose $1.80/month to decay

The 12-month LEAP gives you more time for intrinsic value to materialize, and decay is slower. Over six months, the 12-month LEAP loses $7.20 to theta ($1.20 × 6), while the 6-month LEAP loses $10.80 ($1.80 × 6). The longer expiration preserves more value.

Rule of thumb: Buy LEAPs with 18-24 months to expiration, hold them for 12-18 months, then roll before decay accelerates in the final 6 months.

Layering Expirations to Smooth Income

Instead of selling all your covered calls or puts with the same expiration, stagger them across weekly, monthly, and quarterly cycles. This smooths income, reduces the risk of mistiming a single expiration, and lets you adapt as volatility or valuations change.

Example portfolio:

- Stock A: Covered call expiring in 30 days ($3 premium)

- Stock B: Covered call expiring in 45 days ($4 premium)

- Stock C: Covered call expiring in 60 days ($5 premium)

Every two weeks, one position is coming up for renewal. You're never sitting idle, and you're never scrambling to roll five positions at once. This "rolling ladder" approach keeps income consistent and reduces decision fatigue.

Variation for cash-secured puts: Sell puts at three different strikes and expirations. One expires in 30 days (higher premium, closer strike), one in 60 days (moderate premium, mid strike), one in 90 days (lower premium, far strike). If the stock drops, you're building a position gradually at multiple price levels.

The Dead Zone: 45-90 Days

Options with 45-90 days to expiration decay moderately, not fast enough to maximize theta capture, not slow enough to preserve value efficiently. This is the "dead zone" where trades often make little sense.

If you're selling options, you're not capturing the steepest decay. If you're buying options, you're paying more theta per day than a longer-dated contract. The only reason to trade here is if implied volatility spiked and premiums are unusually high, offsetting the suboptimal decay rate.

Exception: If you're rolling an existing position, moving from 30 days to 60 days (through the dead zone) might make sense to avoid weekly expirations or give yourself more time to adjust.

Monitoring Theta Per Position

Track theta for every option in your portfolio. Most brokers display theta in the option chain or position summary. If you're using a spreadsheet, calculate it manually or pull it from a tool like Wall St Yardie.

What to look for:

- Positive theta (selling options): You're collecting income daily. Higher theta = more income per day

- Negative theta (buying options): You're paying for time. Lower absolute theta = less cost per day

- Total portfolio theta: Add up theta across all positions to see net daily income or cost

Example:

- Covered call on Stock A: +0.10 theta = earning $10/day

- Covered call on Stock B: +0.08 theta = earning $8/day

- LEAP on Stock C: -0.04 theta = losing $4/day

- Net portfolio theta: +0.14 = earning $14/day from time decay

If total theta is positive, time is on your side. If negative, you're paying for exposure (which is fine for LEAPs, but watch for decay acceleration as expiration nears).

Rolling Before Decay Accelerates

Don't hold options into the final two weeks unless you want them to expire worthless or get assigned. The last 14 days is where theta goes vertical—premium disappears fast, and small price moves can trigger assignment.

For covered calls and puts: Roll at 21-30 days before expiration. Extend to the next month, capturing fresh premium and resetting the decay clock

For LEAPs: Roll at 6-9 months before expiration. Theta is still slow, but rolling now avoids the steep decay zone ahead

For protective puts: Close or roll at 30-45 days before expiration unless you want to hold the insurance through the final stretch

Rolling resets the theta curve to the slow part, letting you repeat the process indefinitely.

What Could Go Wrong?

- Chasing weekly expirations for fast theta: Weekly options decay fastest, but they also require constant decisions and expose you to sharp price swings. Transaction costs (commissions, bid-ask spreads) can eat half the premium

- Ignoring assignment risk: Selling 7-day options for high theta means high assignment probability if the stock moves against you. You might earn $50 in premium but lose $500 on an unwanted assignment

- Holding LEAPs too long: A 24-month LEAP becomes a 6-month option eventually. If you don't roll, you're paying steep theta for an expiring contract

- Layering too many expirations: Five stocks with weekly calls means 20 expirations per month. You're managing positions constantly, which defeats the purpose of value investing

- Forgetting intrinsic value: Theta optimization doesn't replace valuation discipline. Selling calls at $110 when fair value is $120 captures theta but caps your upside unnecessarily

Mitigations:

- Stick to 30-45 day expirations for income strategies. Weekly options are for traders, not investors

- Set alerts for 21 days before expiration. Roll or close before decay accelerates to dangerous levels

- Layer no more than three expirations per stock. Weekly + monthly + quarterly is manageable. Anything more is overtrading

- Roll LEAPs at 6-9 months remaining to avoid steep decay

- Always check strikes against your valuation bands (see Using Options Around Valuation Bands) before selling for theta

Next Steps

- Check theta for every option in your portfolio. Most brokers display it in the position summary

- Calculate total portfolio theta (sum of all positive and negative theta values)

- Sell covered calls and puts 30-45 days before expiration to capture steep decay

- Buy LEAPs with 18-24 months to expiration to minimize daily theta cost

- Layer expirations across 30, 45, and 60-day cycles to smooth income and decisions

- Set calendar alerts to roll options at 21-30 days before expiration (selling) or 6-9 months (LEAPs)

- Avoid the 45-90 day dead zone unless volatility is unusually high

- Read Advanced Rolling Techniques to master the art of extending positions without losing premium

*Disclaimer: This content is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own research before investing.*