Expiration Selection for LEAPS

Choosing the right expiration date for a LEAPS is as important as picking the stock or strike price. Too short and you risk running out of time before your thesis plays out. Too long and you overpay for time value you don't need. The goal is to match your option's lifespan to your valuation timeline while building in a margin of safety for delays.

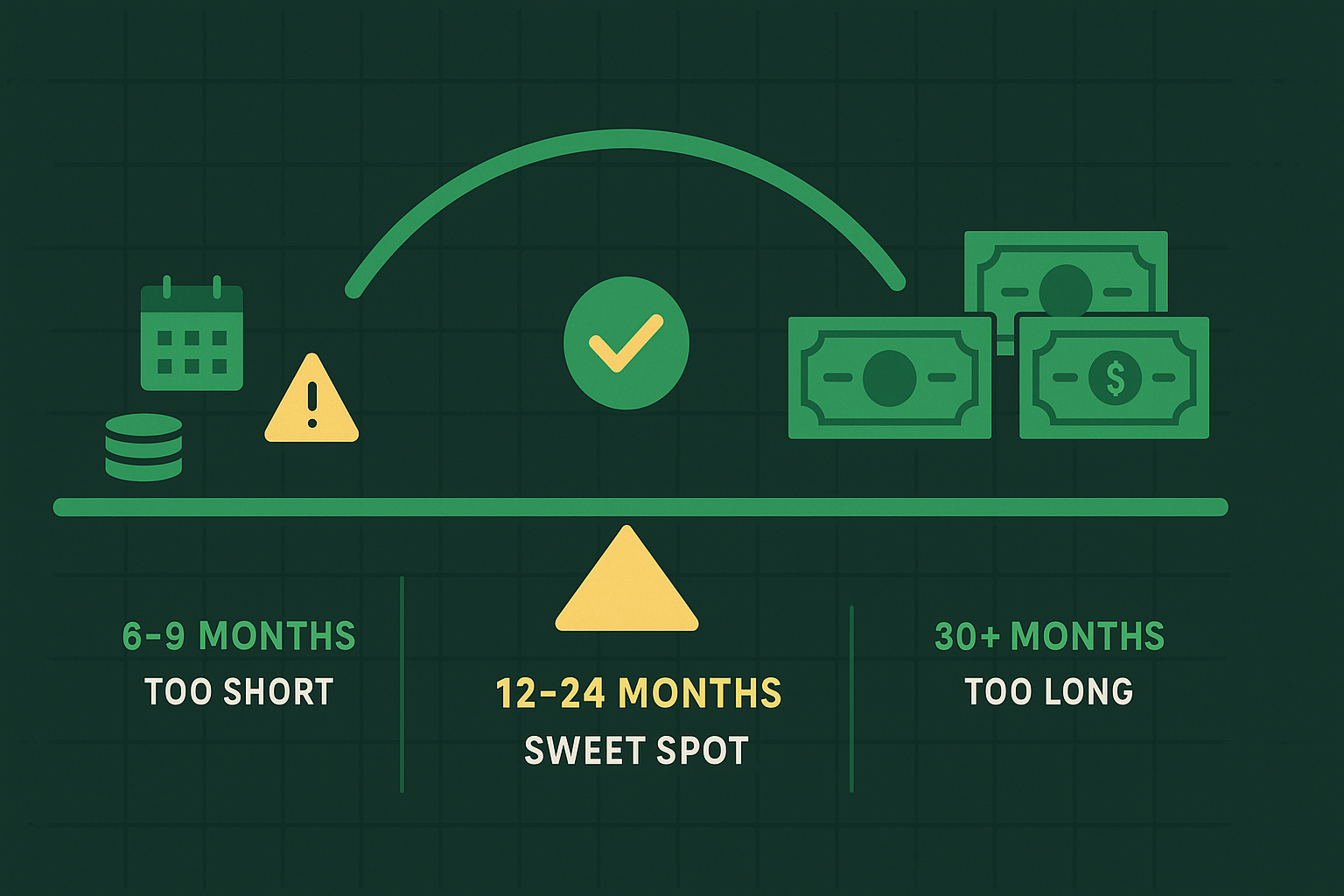

TL;DR

- 12-24 months is the sweet spot: Gives your thesis time to unfold without paying excessive time value

- Match expiration to catalyst timing: If you expect re-rating in 12 months, buy 18-24 month LEAPS for buffer

- Avoid short-dated LEAPS: Anything under 9 months behaves more like a trade than an investment

- Longer isn't always better: 3-year LEAPS cost significantly more with diminishing return on extra time

- Build in a buffer: Add 6-12 months beyond your expected timeline to account for market delays

Why Expiration Matters

Unlike stock ownership, LEAPS have a shelf life. Every contract has an expiration date, and when that date arrives, your option either has value or it doesn't. No extensions, no grace period.

This expiration clock creates two opposing pressures:

- You want enough time for your valuation thesis to play out

- You don't want to pay for more time than you need

Time costs money. The longer the expiration, the higher the premium. A 12-month LEAPS might cost $20, while a 24-month LEAPS on the same stock and strike could cost $28. That extra $8 buys you 12 more months, but is it worth it?

The answer depends on your confidence in timing. If you know a catalyst is coming in six months, a 12-month LEAPS gives you plenty of buffer. If you think the stock is undervalued but have no idea when the market will notice, a 24-month LEAPS is safer.

The 12-24 Month Sweet Spot

For most value investors using LEAPS, expiration dates between 12 and 24 months offer the best balance of time and cost.

Why 12 months works:

One year gives you enough runway for most valuation theses. Earnings reports, product launches, margin improvements, and industry trends typically play out over 6-12 months. A 12-month LEAPS captures this window without overpaying for time.

It also keeps you disciplined. Knowing you have 12 months forces you to think through catalysts and timing. You can't just "hope" the stock eventually goes up like you might with shares.

Why 24 months is safer:

Two years adds a meaningful buffer for delays. Markets don't move on your schedule. A product launch gets pushed back. Management guides conservatively. The industry faces short-term headwinds. All of these can delay your thesis by months, but they don't invalidate it.

A 24-month LEAPS gives you breathing room. If your expected catalyst is 12 months out, buying 24 months of time means you can survive a six-month delay without panic.

The cost difference between 12 and 24 months is usually moderate. You might pay 30-40% more for double the time. That's often a good trade when you're dealing with the uncertainty of market timing.

Avoid going beyond 24 months:

LEAPS with 30+ months to expiration exist, but they're expensive and not worth it for most value strategies. You're paying for three years of time value when most re-ratings happen in 12-18 months. The extra cost eats into your returns.

If you think a stock needs three years to reach fair value, just buy shares and hold them. Don't try to force a multi-year thesis into an options contract.

Matching Expiration to Catalysts

The best way to choose expiration is to work backward from your thesis. Start by asking: why do I think this stock is undervalued, and when will the market recognize it?

Clear near-term catalyst:

New product launching in six months. Buy 12-18 month LEAPS. You have the catalyst plus buffer.

Earnings inflection expected within a year:

Company cutting costs, margins improving over next four quarters. Buy 18-24 month LEAPS. Gives you time to see results plus extra room if guidance is conservative.

Valuation thesis with no specific trigger:

Stock trading at 8x earnings when fair value is 12x, but no obvious reason the market will re-rate soon. Buy 24-month LEAPS or just buy stock. You need maximum time because timing is uncertain.

Industry tailwind accelerating:

Sector recovering from downturn, your company is a leader. Timeline fuzzy but momentum building. Buy 18-24 month LEAPS. Long enough to capture recovery without betting on exact timing.

The key insight: your expiration should always give you more time than you think you need. Markets are slower than you expect. Build in that buffer.

For a deeper dive on the role of catalysts, see choosing the right stocks for LEAPS.

Theta Decay and Expiration

Time decay, or theta, accelerates as expiration approaches. In the first six months of a 24-month LEAPS, decay is slow. Maybe pennies per week. But in the final three months, decay speeds up dramatically.

This means:

- If you buy a 12-month LEAPS, you're entering the accelerated decay zone after nine months

- If you buy a 24-month LEAPS, you have 18-21 months before decay gets painful

Longer expirations give you more time in the "slow decay" phase. This is why even if your catalyst is only 12 months out, buying 18 or 24 months is often smarter. You avoid the panic of watching your option melt in the final months.

If you hold a LEAPS past the 6-month mark and the stock hasn't moved, you face a decision: roll to a new expiration (pay another premium), exercise early (if deep ITM), or let it expire. None of these are ideal, which is why getting the expiration right at the start matters.

For more on how time decay works in long-dated options, read time value in long-dated options.

Cost vs. Time Trade-Off

Here's a rough example of how premiums scale with time:

Stock trading at $100, $80 strike LEAPS:

- 12 months out: $25 premium

- 18 months out: $29 premium

- 24 months out: $32 premium

You pay 16% more to go from 12 to 18 months (50% more time). You pay 28% more to go from 12 to 24 months (100% more time). That's efficient.

But look at this:

- 30 months out: $36 premium

- 36 months out: $39 premium

Now you're paying 44% more for 200% more time. The incremental time gets expensive.

This is why the 12-24 month range is optimal. Beyond that, you're paying more per month of time and getting less value.

What Could Go Wrong?

You pick too short and run out of time:

You buy a 9-month LEAPS thinking the catalyst is six months away. It gets delayed to 10 months. Your option expires worthless even though the thesis eventually works.

Mitigation: Always add 6-12 months of buffer beyond your expected timeline. If you think 12 months, buy 18 or 24.

You pick too long and overpay:

You buy a 36-month LEAPS for safety, but the stock re-rates in 12 months. You paid for 24 extra months of time value you didn't need.

Mitigation: Don't overbuy time. If your catalyst is clear and near-term, stick to 12-18 months. Save the cost.

The stock moves early, but you hold:

The stock hits your target price in six months, but you hold the LEAPS hoping for more. It then falls back, and time decay eats your gains.

Mitigation: Set a target exit price or return. If you hit it early, take profits or roll. Don't get greedy just because you have time left.

You don't monitor as expiration nears:

You buy a 24-month LEAPS and forget about it. At 18 months, the stock is flat but your option is losing value fast. You wake up at 22 months with a melting asset.

Mitigation: Set quarterly calendar reminders to review LEAPS positions. Decide at 12-18 months whether to roll, exit, or exercise.

Market timing betrays you:

Your valuation is right, but a recession or sector rotation delays re-rating by 18 months. Your 12-month LEAPS expires before the recovery.

Mitigation: If the macro environment looks uncertain, buy longer expirations or just buy stock. LEAPS are for conviction plus clarity, not hope.

Real World Example

You're analyzing Company XYZ, a software firm trading at $100 per share. Your DCF model shows fair value at $150. The company is launching a new product line in nine months that should drive revenue growth and margin expansion.

Option 1: Buy a 12-month LEAPS

Premium: $22. Pros: Lower cost, still captures product launch plus three months after. Cons: No buffer if launch delays or market reacts slowly.

Option 2: Buy an 18-month LEAPS

Premium: $26. Pros: Captures launch plus six months for market to recognize impact. Reasonable buffer. Cons: Slightly higher cost.

Option 3: Buy a 24-month LEAPS

Premium: $30. Pros: Maximum buffer, survives delays or slow re-rating. Cons: Paying for time you might not need.

Best choice for a value investor: 18 or 24 months. The extra $4-8 buys meaningful insurance. If the launch happens on schedule and works well, you still profit. If there's a delay or the market is slow to react, you're covered.

Avoid the 12-month option unless you have extreme confidence in both timing and market reaction. The savings aren't worth the risk of running out of time.

Next Steps

- Write down your investment thesis and expected timeline for re-rating

- Add 6-12 months of buffer to that timeline, that's your target expiration

- Compare premiums for 12, 18, and 24-month LEAPS on your target stock

- Calculate cost per month of time: divide premium by months to expiration

- Choose the expiration that gives you adequate buffer without overpaying for excessive time

- Set a calendar reminder for 6 months before expiration to review and decide: hold, roll, or exit

- Use Wall St Yardie to track valuation updates and reassess your thesis quarterly

For a complete framework, see the LEAPS checklist. To understand when LEAPS aren't appropriate, read when NOT to use LEAPS.

*Disclaimer: This content is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own research before investing.*