How Covered-Call ETFs Work: The Simple Version for Stock Investors

Covered Call ETFs promise higher yields than traditional stock funds without requiring you to manage options yourself. But understanding how they deliver those yields helps you decide if the trade-off fits your goals.

Popular Covered-Call ETF Examples

To make this less abstract, here are a few widely followed funds and how they generally approach covered calls:

- JEPI (JPMorgan Equity Premium Income ETF): Uses a U.S. large-cap equity portfolio with an options overlay designed to generate monthly income.

- JEPQ (JPMorgan Nasdaq Equity Premium Income ETF): Similar framework, but focused on Nasdaq-100-style equity exposure.

- QYLD (Global X Nasdaq 100 Covered Call ETF): Tracks Nasdaq-100 exposure and systematically writes call options on that exposure.

- XYLD (Global X S&P 500 Covered Call ETF): Uses S&P 500 exposure with a rules-based covered-call approach.

- DIVO (Amplify CWP Enhanced Dividend Income ETF): Holds a concentrated portfolio of dividend-oriented large caps and writes covered calls tactically on individual names.

These funds all use the same core idea, but they differ in holdings, option-writing rules, fees, and tax treatment. That is why two covered-call ETFs can behave very differently over time.

TL;DR

- Covered Call ETFs own stocks and sell call options: They hold a portfolio of stocks and systematically write calls against those positions

- The options generate premium income: Selling calls creates cash flow that funds monthly distributions

- You give up upside for income: When stocks rally hard, the calls cap gains, but you keep collecting premiums

- Monthly distributions come from premiums plus dividends: The yield often looks attractive but includes selling future growth potential

- Best for income, not growth: Think of these as income generators, not wealth compounders

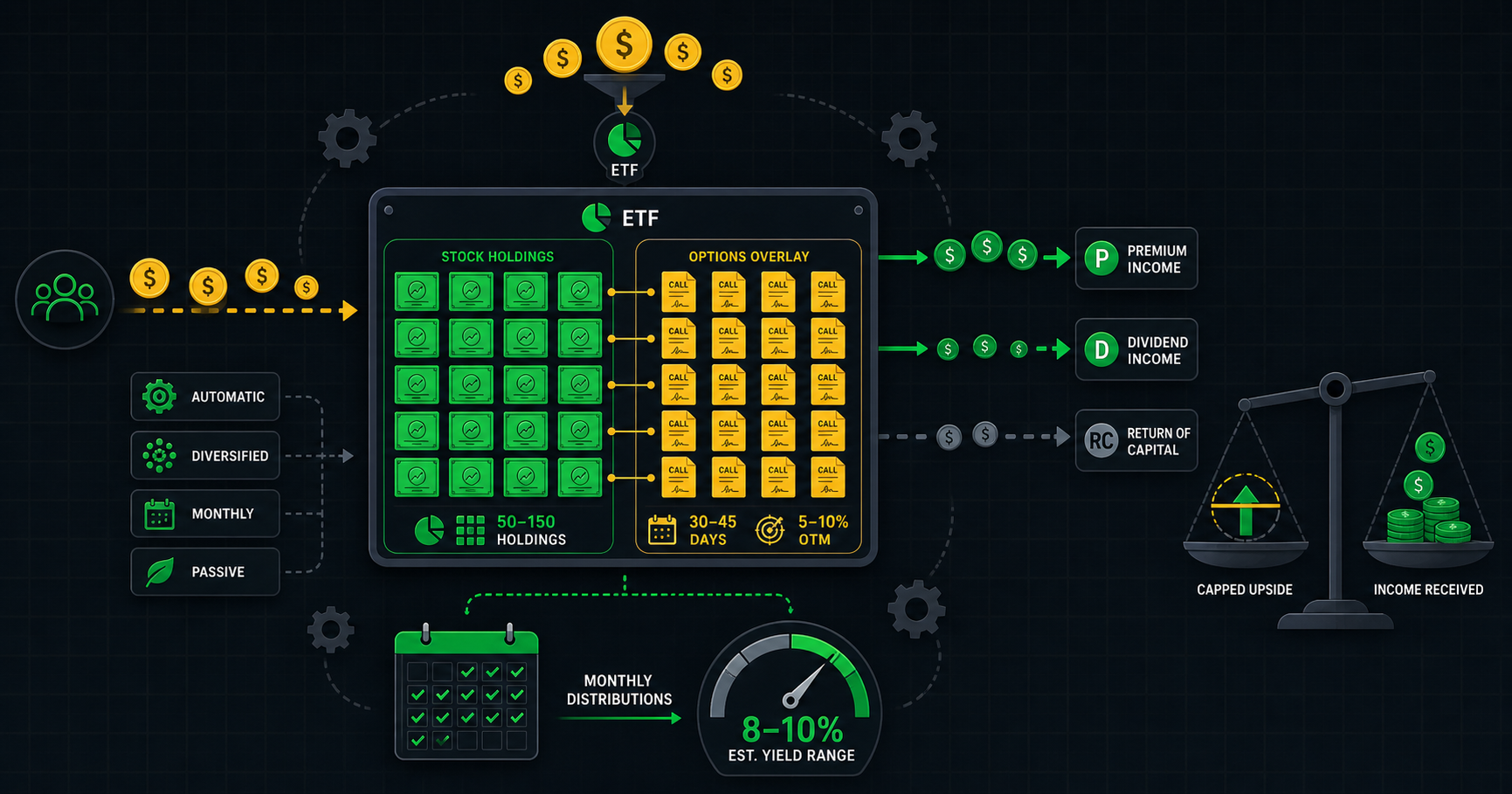

The Basic Mechanics

A covered-call ETF works like a traditional stock fund with one key addition: it sells call options on the stocks it owns.

Here's the process step by step:

Step 1: The fund buys a portfolio of stocks (typically 50-150 companies). These might follow an index like the S&P 500, Nasdaq 100, or a custom selection of dividend-paying stocks.

Step 2: The fund sells call options on these stocks. For example, if the fund owns 10,000 shares of a $100 stock, it might sell 100 call option contracts at a $105 strike price expiring in 30 days.

Step 3: The fund collects premium income from selling those calls. If each contract brings in $200 premium, that's $20,000 in immediate income for the fund.

Step 4: The fund distributes this premium income (plus any stock dividends) to shareholders monthly. This creates the headline yield you see advertised.

Step 5: If stocks rise above the strike prices, the calls get exercised, and the fund sells those shares at the strike price. It then buys new stocks and repeats the process.

The whole system runs automatically. You just buy shares of the ETF and collect monthly distributions.

A Real Example with Numbers

Let's walk through one complete cycle using realistic numbers.

Fund portfolio: 100 different stocks, average price $80/share Total assets: $100 million (holding about 1.25 million shares) Action: Fund sells call options on all positions, strikes set above current prices Expiration: 1 week to 30 days depending on the fund Total premiums collected: $800,000 (about 0.8% of portfolio value in one month)

Scenario 1 - Market stays flat or declines slightly:

- Calls expire worthless

- Fund keeps all premium income: $800,000

- Plus stock dividends: $150,000

- Total monthly income: $950,000

- Distributed to shareholders: 0.95% monthly yield (about 11.4% annualized)

- Next month: Repeat the process

Scenario 2 - Market rallies 8%:

- Many calls get exercised as stocks rise above strikes

- Fund sells those stocks at strike prices (5% gain)

- Keeps the premiums: $800,000

- Capital gains on sold stocks: $400,000

- Total income: $1,200,000

- But: Fund misses the additional 3% gain above the strike prices

- Fund buys replacement stocks at new higher prices

- Next month: Premiums might be higher (due to higher stock prices) but upside remains capped

The key insight: in rising markets, you capture some gains (up to the strike) plus premium income, but you miss the excess upside. In flat or declining markets, the premium income cushions losses.

Where the Yield Comes From

When you see a covered-call ETF advertising 8-12% yields, that income comes from three sources:

Option premiums (majority of yield): This is the cash collected from selling call options. In high-volatility periods, premiums increase, boosting yields. In low-volatility periods, premiums shrink.

Stock dividends (secondary source): The underlying stocks pay dividends, which flow through to ETF shareholders. This might contribute 1-3% to the total yield.

Return of capital (sometimes): If the fund's NAV declines (because capped calls prevented capturing upside), part of your distribution might actually be your own capital coming back to you. This isn't new income but rather money moving from one pocket to another.

Always check the fund's distribution breakdown. Real yield comes from premiums and dividends. Return of capital means you're slowly liquidating your position and they are just giving you your money back.

The Trade-Off: Income vs Growth

The core trade-off is simple but important: you exchange unlimited upside for predictable income.

Traditional stock fund:

- You own stocks

- You capture all gains if stocks rise

- You suffer all losses if stocks fall

- You get dividends (typically 1-2%)

- Your wealth compounds with stock appreciation

Covered-call ETF:

- You own stocks through the fund

- You capture gains only up to the call strike prices

- You suffer most losses if stocks fall (premium income provides small cushion)

- You get premiums plus dividends (typically 7-12%)

- Your wealth compounds primarily through income, less through appreciation

Think of it this way: in a strong bull market, a regular S&P 500 fund might return 20%. A covered-call S&P 500 fund might return 12% (capped gains plus premium income). You gave up 8% growth for higher monthly cash flow.

In a sideways market where stocks go nowhere for a year, the regular fund returns 2% (dividends only). The covered-call fund returns 10% (premiums plus dividends). You captured 8% more income while others waited.

When Covered-Call ETFs Perform Best

These funds shine in specific market conditions:

Sideways markets: When stocks trade in a range for months, traditional investors earn dividends only. Covered-call funds collect premiums month after month without giving up growth (because there isn't any).

Mildly bullish markets: If stocks rise 5-8% annually, the fund captures most of that gain (calls typically struck 5% out) plus premium income. You get 12-15% total returns without much sacrifice.

High-volatility environments: When implied volatility spikes (fear and uncertainty), option premiums increase dramatically. The fund collects fatter premiums, boosting yields. This often happens during uncertain markets where traditional funds struggle.

Income-focused portfolios: Retirees or income investors who need monthly cash flow benefit from predictable distributions. The yield often beats bonds or dividend stocks.

When Covered-Call ETFs Underperform

These funds lag in other conditions:

Strong bull markets: When stocks rip higher 20-30%, covered-call funds cap gains around 10-15% (small appreciation plus premiums). You miss half the rally.

Sustained growth trends: In multi-year bull runs (like 2010-2021), compounding stock gains vastly outperform capped returns. A regular fund might triple while the covered-call fund doubles.

Low-volatility periods: When markets are calm and option premiums shrink, the fund's yield advantage disappears. You're left with dividend-like income but capped upside.

Declining markets: If stocks fall 20%, premium income might offset 3-5% of that loss. You still lose 15-17%. The income cushion helps but doesn't prevent losses.

What Could Go Wrong?

NAV erosion over time: In sustained bull markets, the fund's net asset value can drift lower even while distributions continue. Your $100 share price might drop to $90 over five years while you collected $50 in distributions. Total return looks okay, but you're slowly liquidating principal.

Mitigation: Track NAV alongside yield. If NAV declines steadily, you're sacrificing long-term wealth for short-term income. Consider whether that trade-off aligns with your goals.

Tax inefficiency: Monthly distributions create annual tax obligations. If you reinvest distributions, you're paying taxes on money you didn't actually spend. Return-of-capital portions complicate basis tracking.

Mitigation: Hold these funds in tax-advantaged accounts (IRA, Roth IRA). If held in taxable accounts, understand the tax drag before committing.

Hidden fee drag: Expense ratios (often 0.35-0.6%) plus internal trading costs reduce your effective yield. If the fund advertises 9% yield but charges 0.5%, you net 8.5%.

Mitigation: Compare net yields after fees. Lower-cost funds or DIY strategies might deliver better after-fee returns.

Selling calls on overvalued stocks: If the fund follows an index, it might write calls on expensive stocks alongside cheap ones. You're capping upside on companies that might not deserve it.

Mitigation: Research the fund's holdings. If 40% of the portfolio looks overvalued by your standards, consider whether the overall yield justifies owning those positions.

Comparing to DIY Covered Calls

The ETF approach differs from managing your own covered-call strategy:

ETF advantages:

- Zero management required

- Instant diversification across 50+ stocks

- Professional option execution

- Consistent monthly distributions

- No learning curve needed

DIY advantages:

- Choose only quality stocks you've analyzed

- Sell calls at strikes based on your fair value estimates

- Control assignment and rolling decisions

- Avoid fees (fund expense ratios)

- Better tax treatment of premiums and gains

If you're a disciplined value investor who wants to optimize every decision, running your own covered-call strategy makes more sense. If you want passive income without ongoing work, ETFs deliver that.

Next Steps: Before Buying a Covered-Call ETF

- Review the fund's holdings: Make sure you'd be comfortable owning those stocks without the covered-call overlay

- Check historical NAV performance: See if net asset value has held up or eroded over time

- Compare distribution sources: Look at how much comes from premiums vs. dividends vs. return of capital

- Calculate after-fee yields: Subtract expense ratios from headline yields to get real returns

- Understand the index or strategy: Know whether the fund tracks the S&P 500, Nasdaq, or uses custom selection

- Evaluate tax implications: Decide whether to hold in taxable or tax-advantaged accounts

- Study market conditions: Determine if current volatility supports attractive premium income

- Learn the basics: Review what covered calls are so you understand what the fund is doing

- Consider alternatives: Compare to DIY covered calls and traditional dividend stocks

Covered-call ETFs work exactly as advertised. They generate income by selling call options on stock portfolios, creating consistent cash flow at the cost of capped upside. Whether that trade-off fits your goals depends on your time horizon, income needs, and willingness to sacrifice growth potential for monthly distributions.

If you need income now and don't want to manage positions yourself, they solve a real problem. If you're building long-term wealth and care about compounding, traditional stock ownership or selective DIY covered calls might serve you better.

The mechanics are straightforward: own stocks, sell calls, collect premiums, distribute income. The strategic question is whether you want to optimize for monthly cash flow or long-term growth. Keep the riddim steady, and choose the approach that matches where you're headed.

*Disclaimer: This content is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own research before investing.*