Scaling Cash-Secured Puts Strategically

Most investors make the same mistake: they sell one put contract, get assigned, and suddenly own 100 shares at whatever price the market chose. Scaling changes this. Instead of betting everything on one strike and one expiration, you layer multiple puts at different prices and times, building your position gradually while collecting premiums at every step.

TL;DR

- Layer multiple puts at different strikes: Sell puts at 5-10% intervals below current price to capture multiple entry points

- Stagger expirations: Use 30, 60, and 90-day puts to spread risk and collect premiums continuously

- Average down strategically: Each assigned put lowers your cost basis, turning volatility into opportunity

- Match capital to conviction: Scale position size based on valuation, put 2-3x more capital into deeply undervalued stocks

- Track total exposure: Never commit more than 20-30% of your portfolio to a single stock across all contracts

Why Scaling Beats Single Entry

When you sell one cash-secured put, you're making a binary bet: either the stock stays above your strike or you own 100 shares at that exact price. If the stock drops 20%, you own shares at a price that's now 20% above market. If it rises 10%, you collect the premium but miss the upside.

Scaling solves both problems. By selling multiple puts at different strikes, you get multiple bites: premium income if the stock stays flat or rises, partial assignment if it drops moderately, and full assignment (at lower average prices) if it drops hard. Each contract works independently, letting you adjust to changing conditions instead of being locked into one decision.

Think of it like buying a house. You wouldn't offer $500,000 all at once. You'd start at $450,000, then raise to $475,000 if needed, and finally $500,000 only if the house is worth it. Scaling puts works the same way: you offer to buy at $90, then $85, then $80, collecting rent (premiums) at each level while the seller (market) decides which offer to accept.

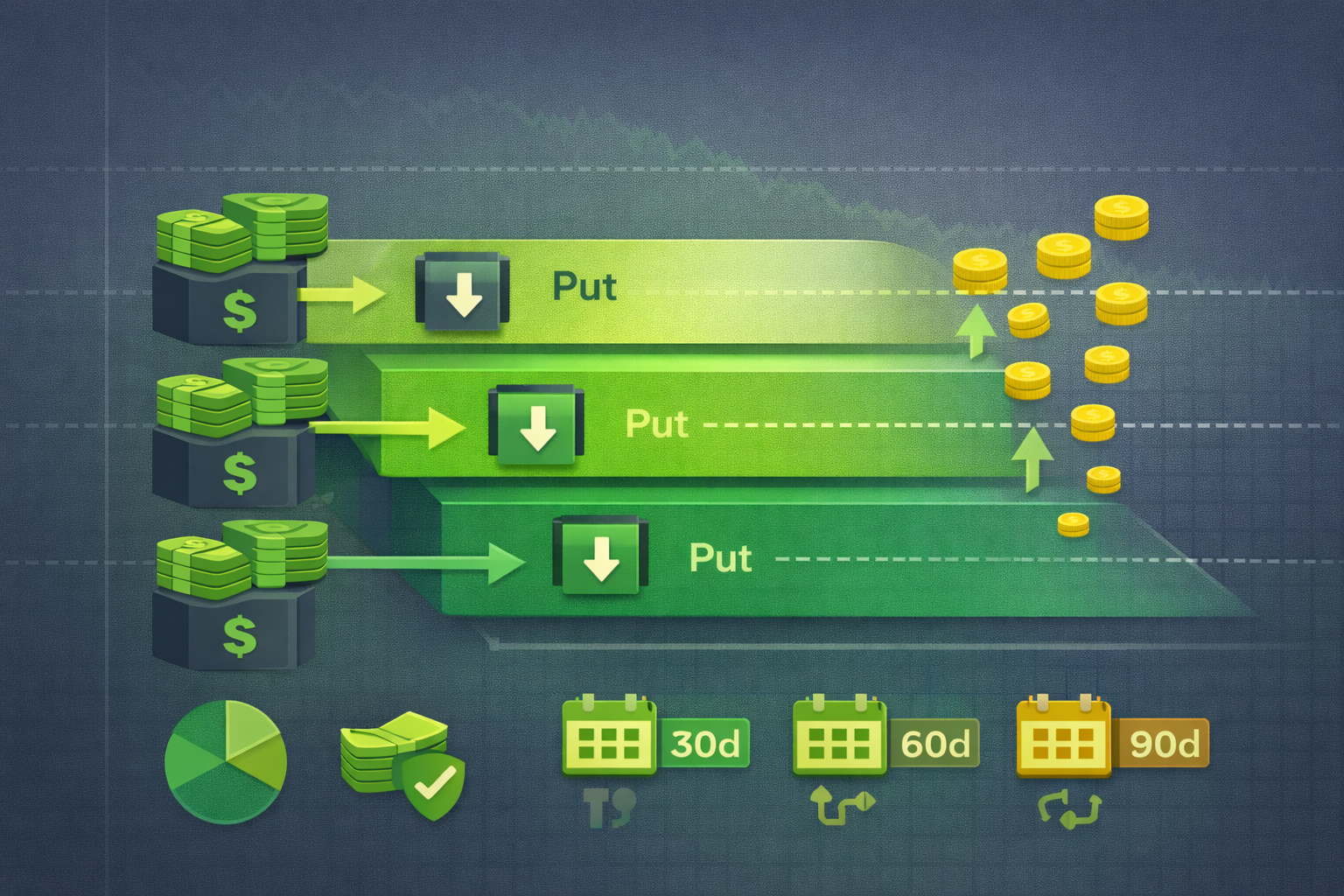

The Basic Scaling Framework

Start with your valuation target. Let's say "QualityCo" trades at $100, but you calculate it's worth $120 based on earnings and cash flow. You'd be comfortable owning shares at $90 (25% margin of safety), but you'd love to buy at $80 or $85 if the market panics.

Here's a three-layer scaling strategy:

Layer 1 (30 days out): Sell 1 put at $95 strike for $3 premium. If assigned, you own shares at $92 net ($95 - $3), an 8% discount to current price and 23% below fair value.

Layer 2 (60 days out): Sell 1 put at $90 strike for $4 premium. If assigned, you own at $86 net ($90 - $4), a 14% discount to current price and 28% below fair value.

Layer 3 (90 days out): Sell 1 put at $85 strike for $5 premium. If assigned, you own at $80 net ($85 - $5), a 20% discount to current price and 33% below fair value.

Total premium collected: $1,200 ($3 + $4 + $5 per share x 100 shares each). You've committed $27,000 in cash ($95 + $90 + $85 x 100 shares), controlling potential ownership of 300 shares.

Now let's see what happens in different scenarios.

Scenario 1: Stock Stays Flat or Rises

QualityCo stays between $95-$105 for three months. None of your puts get assigned. You keep all three premiums ($1,200), a 4.4% return on committed capital in 90 days (about 18% annualized). You're free to sell new puts at similar or higher strikes, continuing the income stream.

This is the best outcome for scaling: you collect rent without tying up capital in shares, and you can repeat the process quarterly.

Scenario 2: Moderate Drop (to $88)

The stock drops to $88. Your $95 put expires in the money, you're assigned 100 shares at $95. Net cost: $92 per share after premium. Current price: $88. You're down $4 per share ($400 unrealized loss) on this position.

Your $90 and $85 puts expire worthless (stock is above their strikes). You keep those premiums ($900). Net result: $900 premium income minus $400 paper loss = $500 ahead, plus you own 100 shares of QualityCo at $92, 23% below your $120 fair value target.

Now you can sell a covered call at $95 or $100 strike to collect more premium while you wait for the stock to recover. You've turned volatility into a discounted entry.

Scenario 3: Big Drop (to $78)

The market panics, QualityCo drops to $78. All three puts get assigned. You now own 300 shares:

- 100 shares at $92 net (from $95 strike)

- 100 shares at $86 net (from $90 strike)

- 100 shares at $80 net (from $85 strike)

Average cost: $86 per share. Current price: $78. You're down $8 per share across 300 shares ($2,400 unrealized loss). But here's the key: you're still 28% below your $120 fair value estimate. The fundamentals didn't change, earnings are still strong, you just got an even better deal than planned.

Compare this to buying 300 shares at $100 outright. You'd be down $22 per share ($6,600 loss). By scaling, you saved $4,200 in downside and collected $1,200 in premiums along the way.

Now you can hold, sell covered calls at $85-$90 strikes to generate income, or even sell more puts at $75 if you believe the value thesis is intact. Scaling gave you options (pun intended).

Advanced Scaling: Conviction-Based Sizing

Not every stock deserves equal scaling. Match your layer sizes to your conviction and valuation gap.

High conviction (40%+ undervalued): Scale aggressively with 2-3 contracts per layer. If QualityCo is worth $140 and trades at $100, sell 2 puts at $95, 2 at $90, 2 at $85. You're building a 600-share position if fully assigned, because the margin of safety justifies it.

Medium conviction (20-30% undervalued): Use 1 contract per layer (standard scaling).

Low conviction (10-20% undervalued): Sell just 1-2 puts total at your highest acceptable strike. Don't layer deeply unless the discount improves.

This approach aligns capital with opportunity. You put more money into the best ideas and less into marginal ones. Use tools like Wall St Yardie to calculate fair value quickly and decide which stocks deserve aggressive scaling.

Timing Your Layers: Expiration Strategy

The example above used 30, 60, and 90-day expirations. This spreads assignments over time, giving you flexibility. But you can adjust based on market conditions:

High volatility (IV is high): Sell shorter expirations (7-30 days) to capture inflated premiums. Chain multiple short-dated puts instead of one long-dated one. Example: sell 4 weekly $95 puts over a month instead of 1 monthly $95 put. Collect more total premium and adjust strikes weekly.

Low volatility (IV is low): Extend to 60-90 days. Premiums are smaller, so you need more time to justify the commitment. Longer expirations also give the business more time to deliver earnings and close the valuation gap.

Earnings approaching: Avoid scaling into earnings unless you're comfortable with assignment. Sell puts after earnings when IV collapses and you can reassess fundamentals.

Defensive Scaling: The Safety Net

Scaling isn't just for building positions, it's also for managing risk. Let's say you already own 100 shares of QualityCo at $95, but you're worried about a short-term drop. Instead of selling all your shares or buying protective puts (expensive), you can scale out using covered calls and add safety with layered puts below your position.

Sell 1 put at $90 (collect $4 premium). If the stock drops to $85, you're assigned another 100 shares at $90, lowering your average cost from $95 to $92.50. If it doesn't drop, you keep the $400 premium, which offsets unrealized losses.

This "scaling down" approach works during corrections. You're willing to double down at lower prices, and premiums help cushion the blow.

What Could Go Wrong?

Scaling isn't risk-free. Here are the pitfalls and how to avoid them:

Over-commitment: Selling 5 puts on one stock ties up $45,000-$50,000 in cash. If you're assigned on all of them, you own a huge position in one company. Mitigation: never commit more than 20-30% of your portfolio to a single stock across all contracts. Diversify across 3-5 stocks if scaling aggressively.

Assignment at the worst time: All your puts get assigned during a crash, and the stock keeps dropping. You're now underwater on 300 shares. Mitigation: only scale into high-quality businesses with strong balance sheets and earnings. If fundamentals deteriorate (debt spiking, earnings collapsing), stop scaling immediately.

Missing the upside: You sell puts at $95, $90, $85, but the stock jumps to $110. None get assigned, you collect premiums but miss a 10% gain. Mitigation: accept this as the trade-off for downside protection. You're prioritizing safety over chasing every rally. Consider selling fewer puts (1 instead of 3) if you expect near-term strength.

Cash drag: Committed capital earns nothing while waiting for assignments. If the stock stays flat for months, your money is tied up. Mitigation: keep 30-40% of your portfolio in liquid reserves. Only commit cash you don't need for 3-6 months.

Changing thesis: You scale into QualityCo at $95, $90, $85, but new information (competitor launches better product, regulatory issues) invalidates your $120 fair value. Mitigation: review fundamentals monthly. If the thesis breaks, let existing puts expire or roll them up/out, don't add new layers.

Real Example: Scaling Into Value

Let's walk through a real trade structure using "RetailCo," a solid company trading at $80 with a fair value of $100 (20% undervalued).

Month 1:

- Sell 1 put at $77 strike, 30 days, $2.50 premium. Net entry: $74.50.

- Sell 1 put at $75 strike, 60 days, $3 premium. Net entry: $72.

- Committed: $15,200. Premium collected: $550.

Month 2:

- Stock drops to $76. The $77 put expires in the money, assigned at $77. After premium, you own 100 shares at $74.50. Current unrealized loss: $150 ($76 - $74.50 x 100).

- $75 put still active with 30 days left.

- Sell covered call at $80 strike, 30 days, $1.50 premium to offset loss.

Month 3:

- Stock recovers to $79. $75 put expires worthless, keep $300 premium.

- Covered call expires worthless, keep $150 premium.

- You now own 100 shares at $74.50 net, stock is at $79. Unrealized gain: $450 ($79 - $74.50 x 100).

- Total premiums collected: $550 (puts) + $150 (call) = $700.

- Total profit: $450 unrealized + $700 realized = $1,150 (15% return on committed capital in 3 months).

By scaling, you controlled the entry price, generated income from premiums, and ended up with shares below fair value. If the stock had dropped to $70, you'd own 200 shares (from both puts) at an average of $73.25, still 27% below your $100 target.

Next Steps

Scaling cash-secured puts is an advanced technique that requires discipline and tracking. Here's how to implement it:

- Start small: Scale with 2-3 contracts on one stock before expanding. Learn how assignments and premiums work in practice

- Use a tracking spreadsheet: Record every put strike, expiration, premium, and net cost basis. Update it weekly to avoid over-commitment

- Focus on quality: Only scale into businesses you'd happily own for 2-3 years. Read Choosing the Right Stock for Puts for selection criteria

- Layer conservatively at first: Start with $5 strike intervals (e.g., $95, $90, $85) instead of $2-3 intervals. Tight layers require more capital and discipline

- Review monthly: Check if fundamentals still support your fair value estimate. If not, stop scaling and exit existing positions

Scaling turns options from a one-time bet into a systematic position-building strategy. It's how professional value investors use puts to buy wonderful companies at discounts while collecting income along the way. Keep the riddim steady, layer your entries, and let the market come to you.

*Disclaimer: This content is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own research before investing.*