Portfolio Allocation for Income Strategies

Knowing how to generate income with options is only half the equation. The other half is deciding how much of your portfolio should focus on income in the first place. Allocate too little and you leave money on the table. Allocate too much and you sacrifice growth, flexibility, or safety. Finding the right balance requires understanding your goals, timeline, and tolerance for complexity.

TL;DR

- Start conservative with 20-30% of your portfolio allocated to income strategies

- Match allocation to life stage: younger investors favor growth, older investors favor income

- Keep cash reserves of 15-25% for flexibility and opportunity capture

- Diversify income sources: mix covered calls, cash-secured puts, and dividend stocks

- Review quarterly and adjust based on market conditions and personal circumstances

The Core Question: Why Income?

Before deciding allocation percentages, understand why you want income in the first place.

Cash flow needs: Some investors need regular income to cover living expenses, fund retirement, or supplement other income sources. For these investors, reliable premium income matters more than maximum growth.

Compounding fuel: Other investors reinvest all income to accelerate compounding. They use option premiums like additional savings contributions, buying more shares or funding new positions.

Risk reduction: Income from covered calls effectively lowers your cost basis, providing a cushion against market drops. Some investors prioritize this psychological and mathematical safety net.

Discipline tool: Selling options forces analysis and decision-making. Some investors find that regular option activity keeps them engaged and disciplined with their portfolios.

Your reason for seeking income shapes how much you should allocate. Cash flow needs demand higher, more reliable allocation. Compounding goals can accept variable income. Risk reduction works even with modest allocation.

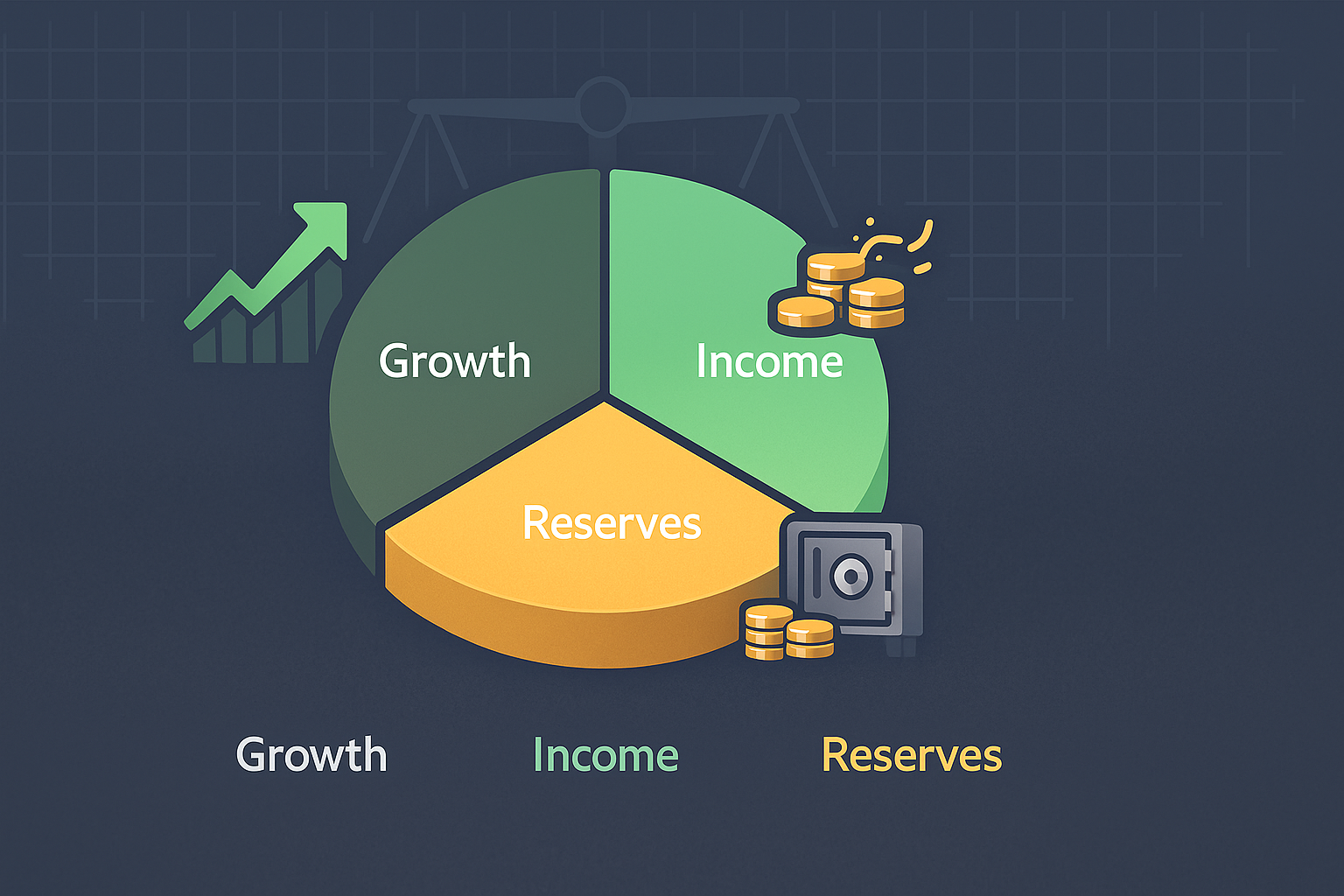

A Framework for Allocation

Think of your portfolio in three buckets: growth, income, and reserves. The percentages shift based on your situation.

Growth Bucket

These are positions you hold for long-term appreciation without options overlay. You believe these stocks have significant upside and you don't want covered calls capping gains. Or they're volatile enough that options risk works against you.

Typical allocation: 30-50% of portfolio

Contents: High-conviction growth stocks, undervalued companies with major upside, positions you're still building

Income Bucket

These are positions actively generating premium income through covered calls or cash-secured puts. The stocks are stable enough for options, and you're comfortable with potential assignment.

Typical allocation: 20-40% of portfolio

Contents: Established value stocks with covered calls, cash reserved for put selling, dividend stocks enhanced with options

Reserve Bucket

Cash and near-cash positions you keep for flexibility. This includes cash to secure puts, emergency funds, and dry powder for market opportunities.

Typical allocation: 15-25% of portfolio

Contents: Cash, money market funds, short-term treasuries

Allocation by Life Stage

Your ideal allocation shifts as you move through different life phases.

Accumulation Phase (Ages 20-45)

You have decades to compound. Growth matters more than income. Premium income should be reinvested rather than spent.

Suggested allocation:

- Growth: 45-55%

- Income: 20-30%

- Reserves: 15-25%

Strategy focus: Use cash-secured puts to build positions at discounts. Sell covered calls sparingly, only on positions approaching fair value. Reinvest all premium income.

Transition Phase (Ages 45-60)

You're shifting from pure accumulation to preparing for eventual income needs. Growth still matters, but income starts contributing meaningfully.

Suggested allocation:

- Growth: 35-45%

- Income: 30-40%

- Reserves: 20-25%

Strategy focus: Increase covered call activity on stable holdings. Build a ladder of put positions across different expirations. Begin treating some premium income as spendable.

Distribution Phase (Ages 60+)

Regular income becomes crucial. Capital preservation matters more. You're drawing down rather than building up.

Suggested allocation:

- Growth: 20-30%

- Income: 40-50%

- Reserves: 25-30%

Strategy focus: Maximize covered calls on dividend stocks. Sell puts conservatively at deep discounts. Prioritize income reliability over yield maximization.

Diversifying Income Sources

Don't rely on a single income strategy. Spread your income allocation across multiple approaches.

Covered Calls

Best for stocks you already own and would hold regardless. Works well in flat or slowly rising markets.

Allocation suggestion: 40-50% of your income bucket

Example: You allocate 35% of your portfolio to income. Covered calls might represent 15% of your total portfolio.

Cash-Secured Puts

Best for stocks you want to own at lower prices. Works well when markets are stable or you're willing to buy on dips.

Allocation suggestion: 30-40% of your income bucket

Example: Puts might represent 12% of your total portfolio.

Dividend Stocks (with optional overlays)

Provides base income independent of options activity. Dividend income flows regardless of market conditions or option expiration outcomes.

Allocation suggestion: 15-25% of your income bucket

Example: Dividend stocks might represent 8% of your total portfolio.

Sizing Individual Positions

Within your income allocation, individual positions matter too.

Rule of thumb: No single stock should represent more than 5-8% of your total portfolio when used for income strategies. This prevents one bad assignment or one stock crash from devastating your income stream.

For put selling specifically, ensure you can handle multiple simultaneous assignments. If you're selling puts on five stocks, all five could get assigned in a market crash. Your cash reserves must cover this scenario.

Use Wall St Yardie to identify quality companies suitable for income strategies. Diversify across sectors and valuation levels.

Adjusting for Market Conditions

Your allocation isn't static. Markets change, and your allocation should adapt.

Bull Markets

Growth outperforms income strategies. Covered calls cap upside you'd rather capture.

Adjustment: Shift 5-10% from income to growth. Sell calls at higher strikes or reduce call-selling frequency. Keep put selling active since assignments are less likely.

Bear Markets

Income provides cushion, but assignment risk increases dramatically.

Adjustment: Shift 5-10% from active income to reserves. Sell puts only at deep discounts. Increase covered call activity since calls provide income during declines.

Sideways Markets

Income strategies shine. Stocks churn without going anywhere, and time decay works in your favor.

Adjustment: Maximize income allocation. Tighten strike prices for higher premiums. Increase trading frequency if comfortable.

Review allocation quarterly or when market conditions shift significantly.

Common Allocation Mistakes

Over-allocating to income too early: Young investors sell covered calls on everything, capping gains during their highest-growth years. Premium income feels great until you realize you've sold away 40% upside on a winning stock.

Solution: Keep at least 40% of your portfolio in growth positions without options overlay until you're within 15 years of retirement.

Under-allocating reserves: Everything is committed to positions or secured for puts. When opportunity appears, you have no capital to deploy.

Solution: Maintain minimum 15% in true cash or near-cash, separate from put-secured amounts.

Concentration in single strategy: All income comes from covered calls on tech stocks. Sector crashes, and income disappears alongside capital.

Solution: Diversify across strategies and sectors. Mix covered calls, puts, and dividend stocks.

Ignoring opportunity cost: You're earning 8% from options income while similar-quality stocks without your overlay are returning 15%.

Solution: Compare total returns, not just income. If growth stocks consistently outperform your income positions, rebalance toward growth.

Sample Portfolio Allocations

Here are three example allocations for different investor profiles:

Young Accumulator (Age 35, $100,000 portfolio)

| Bucket | Allocation | Amount | Strategy |

|---|---|---|---|

| Growth | 50% | $50,000 | High-conviction value stocks, no options |

| Income | 25% | $25,000 | Covered calls on stable holdings, put selling for entries |

| Reserves | 25% | $25,000 | Cash for puts and opportunities |

Expected income: $2,000-3,000 annually from options, reinvested

Mid-Career Transitioner (Age 52, $500,000 portfolio)

| Bucket | Allocation | Amount | Strategy |

|---|---|---|---|

| Growth | 40% | $200,000 | Mix of value and growth positions |

| Income | 35% | $175,000 | Covered calls, puts, dividend stocks |

| Reserves | 25% | $125,000 | Cash and short-term instruments |

Expected income: $14,000-20,000 annually, half reinvested, half set aside

Retiree (Age 67, $800,000 portfolio)

| Bucket | Allocation | Amount | Strategy |

|---|---|---|---|

| Growth | 25% | $200,000 | Conservative growth positions |

| Income | 45% | $360,000 | Heavy covered calls, conservative puts, dividends |

| Reserves | 30% | $240,000 | Cash, bonds, safety cushion |

Expected income: $30,000-40,000 annually, used for living expenses

What Could Go Wrong?

Life circumstances change: You allocated for income but suddenly need liquidity for an emergency. Positions are tied up in options contracts.

Mitigation: Always maintain true reserves separate from put-secured cash. Keep at least 10% completely unencumbered.

Strategy stops working: Market conditions shift and your income strategies underperform for extended periods.

Mitigation: Review results quarterly. If income strategies lag growth alternatives by 5%+ annually over multiple years, rebalance.

Complexity overwhelms execution: You allocate heavily to income but can't manage the positions effectively. Trades get missed, rolls forgotten, assignments mishandled.

Mitigation: Start smaller than you think necessary. Master 3-5 positions before expanding. Complexity should grow with competence.

Next Steps

- Determine your life stage and corresponding allocation targets

- Calculate your current allocation across growth, income, and reserves

- Identify gaps between current and target allocation

- Select income strategies appropriate for your skill level

- Build position diversity across sectors and approaches

- Set quarterly review dates to assess and adjust allocation

- Review portfolio construction principles for strategic guidance

Portfolio allocation for income strategies isn't about maximizing yield. It's about matching your income approach to your goals, timeline, and risk tolerance. Get the allocation right, and income strategies enhance your investing. Get it wrong, and you sacrifice growth or safety for premium income that doesn't compensate for the trade-offs.

Start conservative. Build gradually. Adjust as you learn. That's how disciplined investors integrate income strategies into portfolios that compound wealth for decades.

*Disclaimer: This content is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own research before investing.*